ESG+ Newsletter – 11 June 2026

In this week’s ESG+ Newsletter, we first dive into updates within the sustainable reporting landscape, as Norges Bank Investment Management calls on the European Commission to go further in aligning the ESRS and ISSB standards, enabling companies to satisfy both frameworks within a single report. We also explore a new UN report that reframes AI’s environmental resource footprint as a matter of social justice. On the regulatory front, the FCA has proposed a streamlined approach to climate reporting for investment products, reducing complexity for investors and cutting costs for firms. We then turn to the French SIF’s newly launched VOICE framework, a structured toolkit for assessing the real-world impact of investor engagement. Finally, we examine the latest developments in SFDR 2.0, as EU member states show broad support for revised fossil fuel rules under the updated regulation.

This week’s poll

EU member states broadly support allowing fossil fuel companies in transition-labelled funds under SFDR 2.0, provided they meet certain conditions. Is this the right approach?

|

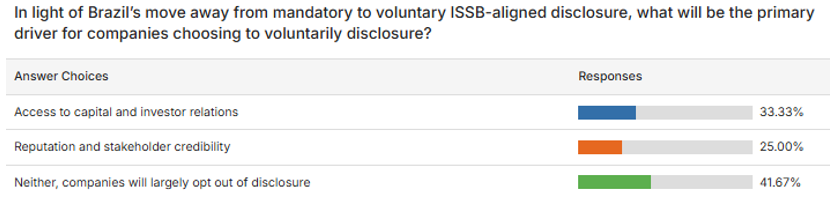

Last week’s poll

Norges Bank Investment Management calls on EU to streamline sustainability reporting

Norges Bank Investment Management (NBIM), the investment manager for Norway’s $2 trillion oil fund, has called on the European Commission to revise sustainability reporting practices, enabling companies to meet the requirements of both the ESRS and ISSB standards in a single report, according to ESG News. Responding to the Commission’s consultation on the revised European Sustainability Reporting Standards (ESRS), NBIM suggests that closer alignment of the standards would enable investors to easily compare sustainability information across companies and countries and reduce the strain of dual reporting. Commenting on NBIM’s consultation response, Carine Smith Ihenacho, Chief Governance and Compliance Officer, said, “We believe a few targeted reforms can deliver this and companies, investors and European capital markets all stand to gain.” The EU Commission’s consultation follows last month’s new draft ESRS, one of the final major steps in the Commission’s initiative to simplify sustainability reporting requirements for companies. NBIM supported the Commission’s efforts to simplify the ESRS and urged the Commission to go further in aligning the standards with the ISSB standards.

New UN Report reframes AI’s environmental impact as also a social issue

AI’s rapid expansion carries a high and often invisible environmental and social cost. A report from the UN University Institute for Water, Environment and Health has quantified the carbon, water, and land footprints tied to the electricity used to train, deploy, and operate AI systems at scale. A critical finding is that low-carbon electricity is not automatically low-water or low-land usage; these footprints do not move in lockstep.

Crucially, the report reframes AI’s environmental impact as a social justice issue also. The benefits of AI often flow across borders and sectors, while the environmental and social burdens can be concentrated in specific communities and regions. For example, AI hardware relies on critical minerals whose extraction and processing can cause environmental and social harms, often concentrated in the Global South and in places with weak oversight. At the end of life, poorly managed e-waste can expose frontline communities to hazardous substances.

The report calls for a responsible AI ecosystem grounded in transparency, efficiency by design, equity and environmental justice, lifecycle responsibility, and global cooperation, ensuring that technological innovation does not simply shift its costs onto the world’s most vulnerable.

FCA proposes streamlined climate reporting rules for investment products

On June 5, the UK Financial Conduct Authority (FCA) published its latest Quarterly Consultation Paper, within which was a proposed simplification of climate-related reporting requirements for investment products. The proposal would replace standardised climate reports for individual investment products with a more flexible system, designed to give ordinary investors more concise information while preserving essential emissions data for institutional clients and reducing reporting costs for firms. Under rules introduced in 2021, firms must publish annual reports based on the Task Force on Climate-related Financial Disclosures (TCFD) framework. These reports include information such as carbon-emissions metrics and analysis of how investments may perform under different climate-based scenarios. An FCA review found that the rules had aided firms in considering the full extent of climate risks, but that detailed reports were underutilised, often viewed as too complex by investors.

The proposed change would therefore replace these reports with a more targeted approach. Retail investors are to receive clearer information on where climate risks or opportunities could affect an investment’s financial performance, while institutional clients, such as pension trustees, would be able to request key emissions data directly from firms. According to reporting by ESGtoday, the proposal would not remove all climate-reporting obligations, with annual entity-level reporting requirements remaining in place. The FCA estimates that the changes could save firms around £20 million annually. Consultation is open until July 13th, with the FCA aiming to implement the changes in autumn 2026.

French SIF launches a new framework to assess investor engagement

According to Net Zero Investor, the French Sustainable Investment Forum (SIF) has launched a new framework aimed at assessing the impact of investor engagement. The initiative is intended to help asset owners assess asset managers’ stewardship credentials more consistently. Alongside the framework, the French SIF has introduced the VOICE (Valuation of Influence in Corporate Engagement) toolkit to evaluate and compare engagement practices.

Investor engagement has become an increasingly important mechanism for driving corporate change. However, measuring its effectiveness remains difficult due to the lack of widely accepted definitions and measurement standards. Many asset managers still report engagement activity through the number of company meetings or voting decisions rather than demonstrating tangible outcomes. As a result, asset owners are increasingly seeking clearer evidence that engagement efforts are influencing company behaviour and delivering meaningful results.

In the new framework, engagement is defined as “the practice whereby investors engage in an iterative and deliberate cycle of interactions with the companies in which they invest. Engagement is based on one or more specific and targeted objectives, with the aim of influencing companies’ transparency, operations, and/or strategies on environmental, social and governance (ESG) issues, and with the aim of protecting and/or enhancing long-term value creation.” The VOICE toolkit complements this by assessing investor influence through a five-level scale ranging from “no influence” to “recognised influence,” where a company acknowledges the investor’s contribution to a measurable change. Between these two extremes, a range of indicators can be used to provide evidence of influence.

Asset managers seeking to strengthen their position in the French market may soon need to adapt to this more outcome-focused approach to engagement reporting, as stewardship credentials are likely to play an increasingly important role in mandate selection. The French SIF also plans to promote the framework more widely across Europe through a proposed roadshow currently under discussion. Its uptake and practical impact will be closely watched in the months ahead.

EU member states support revised fossil fuel rules under SFDR 2.0

EU member states are broadly supportive of modifying how fossil fuel companies can be included in funds classified under the Transition category of the updated Sustainable Finance Disclosure Regulation, Responsible Investor reports. Under the current proposal, transition funds would not be allowed to include investments in fossil fuel companies. However, a compromise has been suggested which would permit such companies to remain eligible for these funds, so long as they commit a defined share of their capital expenditure, most likely toward activities aligned with the EU taxonomy. Based on an early outlook, it appears this figure will fall between 15% and 20%. In addition, fossil fuel companies included within such funds would also need to publish a credible plan to reduce Scope 1 and Scope 2 emissions. To add further clarity to what transition funds containing fossil fuel companies hold, it has also been proposed by the Cyprus presidency, the current acting president of the EU Council, that these funds will have to release mandatory annual disclosures detailing the proportion of their investments which sit within fossil fuel companies. The Cyprus presidency is aiming to reach a formal negotiating position before its term concludes, with a vote on the SFDR approach expected in September of this year.

ICYMI

- Major Irish companies face significant compliance, enforcement and reputational risks because they have taken their eye off the ball on the EU’s new corporate sustainability legislation, according an Irish Independent article.

- Activist investors have made a record number of proposals to Japanese firms for shareholders to vote on at annual general meetings this month, including growing calls for company executives to step down, Reuters reports.

| The views expressed in this article are those of the author(s) and not necessarily the views of FTI Consulting, its management, its subsidiaries, its affiliates, or its other professionals.

©2026 FTI Consulting, Inc. All rights reserved. www.fticonsulting.com |