ESG+ Newsletter – 5 June 2025

This week’s newsletter covers a lot of ground, including analysis of shareholder proposals and a debate on federal versus state legislation in the US. We also review the latest view of ESG as a concept, dive into the impact of fund renaming and look at changes to the UK’s Stewardship Code.

This week’s poll

Are electric vehicle mandates central to the goal of decarbonisation and energy transition?

- Yes

- No

- The cure may be worse than the disease

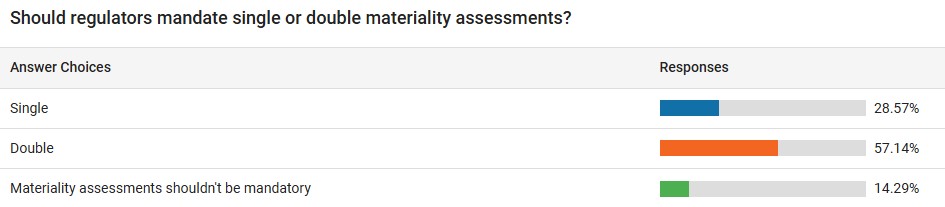

Last week’s poll results

Corporate political spending proposals lead ESG support in 2025 proxy season

In a year of waning support for environmental and social (E&S) proposals, Responsible Investor highlights that shareholder resolutions related to political contributions have emerged as the most successful during US proxy season. The five successful resolutions – all submitted by the same individual – urged companies to disclose their policies on political contributions, including details on recipients and the executives responsible. Four additional proposals gained over 30% shareholder support. This trend follows a similar pattern from 2024, when one of the three ESG proposals to secure majority support focused on election spending disclosure, with the two others targeting greenhouse gas emissions. As the political landscape rapidly evolves, investors are open to demanding greater transparency on political spending.

According to Morningstar Sustainalytics, covered in the Responsible Investor piece, political spending disclosure accounted for nearly half of the E&S proposals with at least 30% support this year. Out of 19 resolutions meeting this threshold so far, nine addressed political contributions, while the remaining 10 focused largely on social issues. In stark contrast, 45 proposals filed by anti-ESG groups averaged just 1.8% support. As ESG scrutiny intensifies, transparent political engagement is a priority that shareholders feel comfortable supporting.

UK FRC to streamline Stewardship Code

The Times has reported on the latest update to the UK Stewardship Code, a “City code”, overseen by the UK’s accounting watchdog the Financial Reporting Council (FRC), seeking to reduce the number of reporting requirements for investors. While the Code is voluntary, it is used to show how fund managers engage with companies on key issues. Recently though, there has been growing frustration with the increasing length and complexity of reporting requirements. The FRC’s update to the Code comes as the Government presses regulators to consider ways of promoting growth in the economy, by reducing regulatory burdens. The newest version of the Stewardship Code, published this week, includes an amendment to its definition of “stewardship”, which removes references to ESG issues. Another change is the inclusion of a specific reference to proxy voting agencies for the first time, encouraging proxy agencies to publish their methodologies and approach to dealing with and engaging with corporates. Enhanced transparency of proxy agency activity, responsible for advising institutional investors on how to vote in meetings, is likely the result of increasing complaints of their practices from those they opine on, public companies and Boards.

Hundreds of ESG funds renamed as ESMA guidelines kick in

As new guidelines from the European Securities and Markets Authority (ESMA) come into effect, Europe’s fund industry is experiencing a wave of change. As reported by IPE, the rules are designed to combat greenwashing and ensure clarity for investors, setting strict standards for how funds can use ESG and sustainability-related terms in their names. For a fund to include the terms “transition”, “environment”, “social”, “governance”, “impact” or “sustainability”, at least 80% of its assets must be invested in line with environmental or social characteristics or sustainable objectives. These measures are designed to prevent funds from having significant exposure to activities linked to fossil fuels while simultaneously presenting themselves as environmentally focused or “green.” Asset managers are responding in different ways: some are adjusting their investment strategies to keep ESG branding, while others are simply rebranding to comply with the new rules.

The impact has been immediate, with nearly 700 investment funds changing their names to avoid breaching the new rules. 232 funds now promise just “screening” commitments rather than using the ESG labelling. According to campaigners, the stricter standards have already had more than a cosmetic impact, with an estimated €22 billion shifted away from fossil fuel investments from funds seeking to retain their ESG credentials.

What’s in a name? Investors moving away from ESG as a unified concept

Institutional investors are distancing themselves from ESG as a single, overarching framework, reports Bloomberg. These findings come from a recent Morningstar survey of asset owners across North America, Europe, and Asia-Pacific. While the commitment to sustainable investing remains strong, many now view environmental, social, and governance factors as distinct considerations rather than one unified strategy. The survey revealed that the environmental component, especially climate risk, has become the main priority. Asset owners see it as a material investment risk and are focusing more on measurable climate strategies than on broader ESG labels. Many investors believe the term “ESG” has become overly politicised and diluted, leading to concerns about greenwashing and oversimplification. As a result, terms like “sustainable investing” or “responsible investing” are now favoured for their clarity and focus. The report also notes growing caution among asset owners amid global geopolitical tensions. In an uncertain market environment, many are holding off on short-term portfolio changes until more stability and clarity emerge. Overall, the shift suggests a maturing approach to sustainability, less about buzzwords and more about targeted, practical investment decisions.

Senate moves to revoke California’s vehicle emissions waiver

According to ESG Dive, the U.S. Senate recently passed resolutions to revoke California’s authority under the Clean Air Act to set stricter vehicle emissions standards than federal rules. This move targets California’s 2022 Advanced Clean Car II regulations, which require all new cars sold in the state to be zero-emission by 2035. The decision to revoke California’s authority was supported by certain industries which argue the rules are unrealistic and harmful to consumers and the economy.

California, backed by 10 other states, opposes the resolution, and plans to sue to maintain its emissions waiver, citing the state’s long history of battling air pollution and the legal right to protect public health. Clean air advocates warn that rescinding the waiver could lead to poorer air quality, more health problems, and hinder progress toward cleaner transportation. The debate also involves broader issues of states’ rights versus federal authority – something we are seeing across the US when it comes to climate-related and sustainability legislation.

ICYMI

- BRICS agreed on its first climate finance framework, outlining priorities like reforming multilateral development banks and mobilising private capital. The non-binding plan will be submitted for formal approval at a July summit, Environmental Finance reports.

- Vanguard will expand proxy voting choice to 10 million investors, up from 3.5 million, as part of efforts to reduce its direct influence on shareholder elections. According to Reuters. The move brings nearly $1 trillion in assets into its “Investor Choice” program, letting investors select voting policies rather than cast company-specific votes.

- A new European Commission report finds the EU is nearly on track to meet its 2030 climate goals, including a 55% cut in greenhouse gas emissions from 1990 levels.

| The views expressed in this article are those of the author(s) and not necessarily the views of FTI Consulting, its management, its subsidiaries, its affiliates, or its other professionals.

©2025 FTI Consulting, Inc. All rights reserved. www.fticonsulting.com |