ESG+ Newsletter – 20 March 2025

This week’s newsletter reviews developments from a regulatory perspective, including a focus on potential US vs. EU tensions, as well as updates to market practice on climate targets; and AI reporting & oversight. We also analyse whether greater transparency in proxy voting and stewardship is being met with action on ESG integration. Finally, as we approach proxy season in the US, we look at whether the SEC’s view of shareholder proposals is changing.

This week’s poll

Do you think the current debates over ESG will result in more or less contention at 2025 AGMs?

- More

- Less

- No difference

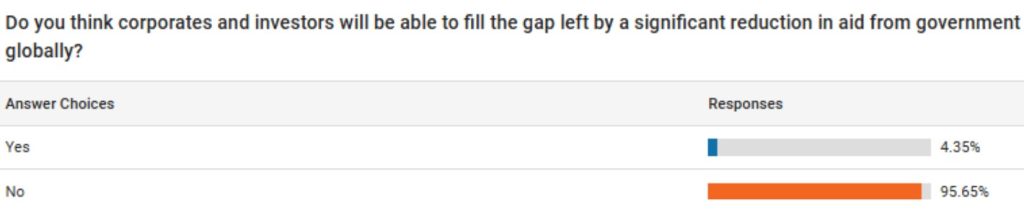

Last week’s poll results

Republicans propose bill to counter EU ESG regulations

Senator Bill Hagerty of Tennessee has introduced legislation that he says is designed to protect American companies from European ESG regulations, as reported by Bloomberg. A Republican member of the Senate Banking Committee, Hagerty argues that EU policies impose unnecessary burdens on US businesses and infringe on national sovereignty. His proposed bill, the Prevent Regulatory Overreach from Turning Essential Companies into Targets (PROTECT USA) Act of 2025, specifically targets the EU’s Corporate Sustainability Due Diligence Directive (CSDDD). This Directive requires large corporations to implement climate transition plans and human rights risks, in their own operations and values chains, placing liability on companies and Directors for ESG violations. In response to opposition, and in an effort to reduce regulatory burdens, the EU recently revised the Directive, removing key provisions such as civil liability for non-EU companies.

Hagerty’s proposal reflects broader Republican resistance to ESG policy, which they claim hurt businesses and reflect ideological overreach. The move follows warnings from some US officials, who have suggested possible trade retaliation against EU regulations. Major US corporations have also expressed concerns over the Directive’s extraterritorial impact. The European Commission, however, insists that the revised rules aim to reduce administrative burdens and take into account feedback from both EU and non-EU stakeholders. More to follow on this one!

Climate group SBTi proposes new rules, holds line on carbon offsets

Amidst waning commitment, as well as increased political and legal pressure on those detailing their climate ambitions, the Science-Based Targets initiative (SBTi) has published guidance on setting quality emissions-reductions plans as part of its Net-Zero Standard. Reuters has reported on the consultation around the guidance, confirming that while companies’ ability to offset “residual” emissions will remain, the widespread use of carbon offsetting is still not endorsed. Instead, companies are encouraged to purchase carbon credits beyond their supply chains; however, the impact of carbon credits continues to attract scrutiny. Supporters suggest they are essential for funding carbon sequestration projects, while critics argue the impact of these projects is immeasurable, inaccurate and fail to deliver on their anticipated environmental benefits. The SBTi also proposed changes to tackling Scope 3/supply chain emissions, including latitude around procurement strategies, guiding companies to focus on the most carbon-intensive activities in the supply chain, and making targets optional for smaller companies. Despite a level of pushback against climate commitments at corporate and legislative level, the SBTi stated that it continues to see exceptional growth in the number of companies setting science-based targets. As a means of trying to maintain momentum, the body is hopeful that their proposed changes will help smaller companies or those from emerging markets to join the large number of companies who have validated their climate targets.

ISS highlights surge in AI Board oversight and shareholder proposals

ISS has published its 2025 AI in Focus Report, highlighting key trends in AI-related corporate governance. The report revealed that the percentage of companies providing some disclosure of Board oversight increased by more than 84% year-over-year and over 150% since 2022. These increases were observed across all industries. In 2024, over 31% of S&P 500 companies disclosed some level of board oversight on AI, which included committee oversight responsibilities, Directors with AI expertise, or the establishment of an AI ethics Board. Among S&P 500 companies, 20% reported having at least one director with AI expertise, while just under 14% disclosed explicit board or committee oversight of AI, and only 2% had a dedicated AI ethics board. Our own research at FTI Consulting looked at the largest 30 companies in the Dow Index and found similar but slightly higher results with 50% of companies disclosing on board oversight, 20% reporting on board committee responsibilities and 23% having at least one director with AI skills. Both the size of the companies in our dataset and the large number of tech companies present most likely influenced why we found higher levels of disclosure. In comparison, we also examined Europe’s 50 largest companies. The findings showed that 46% disclosed some level of Board oversight, with 18% evidencing specific committee oversight, 20% highlighting directors with AI expertise, and 24% reporting when AI was discussed in Board meetings. Our research also analysed additional disclosure categories, including AI policies, senior leadership involvement, knowledge development, audits, risk management, and KPIs and provided real-world examples of how companies approach AI governance.

ISS also flagged the rising number of AI shareholder proposals, which have predominantly targeted TMT companies, demanding greater transparency through reports. Again, FTI Consulting’s research published in September 2024 showed that shareholder proposals were widening to include a consumer services company, and it was also the first-time proposals specifically sought clearer attribution of board responsibilities related to AI. Given the growing sophistication of shareholder demands on AI, as well as the clear risks and opportunities associated with the technology, it’s unsurprising that ISS’ research points to significant changes in how this issue is being managed by corporates, much like the evolving approach to ESG issues previously.

SEC’s stance on shareholder proposals

In the US, companies traditionally utilise no-action requests to seek informal guidance from the Securities and Exchange Commission (SEC) regarding the permissibility of excluding shareholder proposals from proxy materials. These requests typically assert that a proposal is excludable based on various regulatory grounds or shareholder overreach. However, recent SEC decisions, as reported by ESG Dive, provide insight into the agency’s stance on climate-related shareholder proposals. Specifically, the SEC has denied no-action requests from numerous financial institutions seeking to exclude proposals related to climate disclosures, including those concerning clean energy supply ratios. The primary argument made by companies was that such proposals intruded upon ordinary business operations and constituted micromanagement from shareholders. In response the SEC found that the shareholder proposals were valid and did not overstep the mark in terms of shareholder input. Furthermore, the agency has ruled that several shareholder proposals concerning indigenous rights policies are also non-excludable.

While some no-action requests remain pending, and the data reviewed relates to December and January, a period during which the SEC was changing due to the arrival of a new administration, the decisions suggest a continued trend towards requiring companies to include sustainability-related proposals in their proxy materials. Although future regulatory changes or executive actions may affect the breadth of sustainability disclosures, shareholder proposals are poised to drive increased transparency, at least in the near term.

PLSA increases shareholder voting transparency with revised Vote Reporting Template

The UK’s Pension and Lifetime Savings Association has updated its Vote Reporting Template to improve transparency and standardisation in shareholder voting disclosures. Originally introduced in 2020, the template helps asset owners collect and assess voting information from investment managers so that pension fund trustees can demonstrate effective stewardship of their assets. As part of this, they must show how they are leveraging their voting rights to support or sanction the actions of their investee companies. The revised template is a result of work done by the FCA-convened Vote Reporting Group (VRG), which brought together investment managers, pension funds, insurers, companies and NGOs to improve vote reporting quality. Pension schemes play an important role in driving corporate change, and this template aims to boost transparency and accountability for asset owners. By allowing clients to compare voting decisions, the FCA and PLSA note that the revisions should promote sustainable investment practices, which is increasingly in the spotlight, with certain asset managers doubling down on sustainability as a means of attracting capital and mandates.

However, while increased transparency is designed to spur a greater focus on sustainability and stewardship, only 35 large pension funds out of 123 incorporate ESG factors into the portfolio management process, as reported in P&I. While the updated template’s positive impact on voting transparency may increase pressure, pension funds may still lack genuine ESG integration across their investment approaches.

ICYMI

- UK Conservative party leader Kemi Badenoch has rejected the UK’s 2050 net zero target stating that it will either “bankrupt” the country or result in lower living standards, according to Sustainable Views.

- The CFA Institute’s certificate in ESG Investing will be renamed the Sustainable Investing Certificate, Plan Advisor reports.

| The views expressed in this article are those of the author(s) and not necessarily the views of FTI Consulting, its management, its subsidiaries, its affiliates, or its other professionals.

©2024 FTI Consulting, Inc. All rights reserved. www.fticonsulting.com |