Executive Pay in the UK and Ireland: Key Shareholder Voting Trends for 2026

Overview

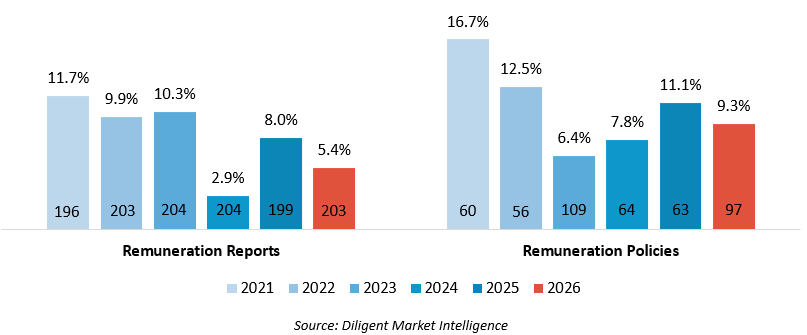

Early 2026 voting data, covering approximately half of FTSE 350 and ISEQ 20 companies through to 31 May, points to improving alignment between boards and shareholders on executive pay, with dissent levels falling between the historic lows of 2024 and the higher levels seen in 2025. As shown in Figure 1, the season saw a decline in instances of significant opposition, defined as 20% or more of against votes, on both remuneration reports and remuneration policies. Strong market performance in 2025 (the FTSE 350 and ISEQ 20 returned 24.1% and 37.4% respectively) and broadly unchanged guidance from the Investment Association (IA), Institutional Shareholder Services (ISS), and Glass Lewis provided a supportive backdrop. Some caution is warranted, however. Close to one in ten companies still faced significant dissent on their remuneration policy in 2026, suggesting a persistent gap between investors and remuneration committees on the most effective means of designing incentive structures. Investors and proxy advisors continue to treat pay practices and disclosures as litmus tests for board-level oversight. Where concerns go unaddressed, the consequences can extend beyond remuneration votes: in 2026, remuneration committee chairs at companies with two consecutive years of significant dissent attracted between 17% and 37% votes against their re-election. Persistent pay dissent can also draw activist attention, providing these actors with a ready-made governance narrative to rally shareholder support.

Figure 1: Proportion of Companies that Faced ≥20% Opposition on a Remuneration Proposal (FTSE 350 & ISEQ 20)

Total number of votes from 1 January to 31 May each year presented at the bottom of the chart

Key Takeaways

- Dissent on remuneration policies remains elevated. The proportion of companies facing significant dissent on remuneration policies declined from 11.1% in 2025 to 9.3% in 2026, though this remains above the level recorded in 2023, when most of these companies last sought shareholder approval for their pay policy. Almost one in ten companies faced significant dissent on their remuneration policy in 2026 – a materially higher proportion than those facing significant dissent on their remuneration report (5.4%). This is consistent with investors generally challenging remuneration structures at the time of the policy vote, while focusing their review of remuneration reports on the actual alignment of pay outcomes with the shareholder experience.

- Restricted shares continue to attract dissent as market practice evolves. In 2026, only one company encountered significant dissent on its remuneration policy by simultaneously introducing restricted shares and increasing variable pay opportunity (down from six in 2025). However, three companies that applied the 50% discount generally expected by IA members (while replacing a portion of their performance shares with restricted shares) still faced significant opposition, driven by concerns over pay design or the rationale for switching structures entirely. As more companies seek shareholder approval to grant restricted shares, this points to remaining disagreements between boards and investors over both the suitability and optimal design of hybrid incentive schemes.

- Dissent on remuneration reports is down, but the same pressure points remain. The proportion of FTSE 350 and ISEQ 20 companies facing significant dissent on remuneration reports declined from 8.0% in 2025 to 5.4% in 2026, supported by strong market conditions in 2025 (the FTSE 350 and ISEQ 20 indices delivered returns of 24.1% and 37.4% respectively). The primary drivers of opposition, largely unchanged from last year, related to significant salary increases and remuneration committees failing to align pay outcomes with shareholder experience and company performance.

- Failure to address dissent on remuneration is impacting board elections and may attract activist attention. Of the 16 companies that encountered significant dissent on their remuneration report in 2025, only four did so again in 2026, reflecting a level of board responsiveness to investor voting. Where dissent has persisted, however, investors have demonstrated a willingness to escalate, with remuneration committee chairs at these companies receiving between 17% and 37% of votes against their re-election. Boards should also be aware that sustained pay dissent can attract third-party activists who will utilise it as evidence of governance failure and a tool to rally other shareholders.

- Get ahead of 2027: proactive engagement is the best defence. As geopolitical and market uncertainty persists, boards face mounting pressure to design remuneration arrangements that effectively incentivise senior leadership (particularly over the long term), attract and retain key talent, and ensure alignment with company performance and shareholders’ interests. Proactive adjustments to remuneration structures are generally viewed more favourably by investors and proxy advisors than recourse to ex-post discretion. Companies that engage early with key stakeholders and disclose material decisions with clarity and purpose will be best placed to mitigate the risk of shareholder dissent in 2027.

Methodology

The primary objective of this paper is to examine how voting outcomes have evolved in 2026. Specifically, the analysis focuses on AGM voting results at FTSE 350 and ISEQ 20 companies during the period from 1 January to 31 May 2026, as well as corresponding proxy voting outcomes from the previous five years. AGM results are based on data from Diligent Market Intelligence obtained from companies’ disclosures. We have considered vote results excluding abstentions (legal basis). We have also defined instances of significant opposition (or dissent) in line with the UK Corporate Governance Code as proposals receiving 20% or more of against votes. We note that the new Irish Corporate Governance Code adopts a higher threshold, defining significant dissent as 25% or more votes cast against a proposal.

To identify the primary drivers of significant dissent, we examined company annual reports, proxy advisor reports, and investor voting rationales available through Diligent Market Intelligence.

Background – Investor Expectations for 2026

The IA’s Principles of Remuneration

On 12 November 2025, the IA issued its annual letter to remuneration committee chairs in the UK, outlining key expectations for the 2026 AGM season. Following a significant revision and simplification of its Principles of Remuneration in 2025, which clarified that investors would provide companies with the flexibility to adopt pay structures suited to their business and strategy, the IA confirmed that no further changes would be made for 2026. The 2025 reforms were substantive enough to warrant a period of embedding, and the focus for 2026 was accordingly set on improving implementation and disclosure rather than introducing new requirements.

The November 2025 letter urged remuneration committees to provide company-specific justifications for material changes in pay rather than generic explanations. Any benchmarking exercise is expected to be clearly detailed, including peer selection and explanations for differences in size, complexity, performance, and the types of pay schemes used by peers. On hybrid pay schemes, where part of the long-term incentive plan (LTIP) is not performance-based, the IA clarified that these should generally be reserved for businesses with substantial US exposure or those competing globally for talent, signalling scepticism toward broader adoption beyond their intended use case of enabling UK issuers to better compete with US companies for talent. More broadly, IA members emphasised the need to demonstrate a clear link between pay and performance, and with inflation and economic uncertainty continuing to affect households, investors also expect companies to explain how they balanced executive reward with outcomes for employees, customers and other stakeholders.

Fidelity International’s Letter to UK Company Chairs

Alongside the IA’s guidance, major asset managers have reinforced these expectations through direct engagement with company boards. In a notable move reported by the Financial Times in December 2025, Fidelity International, which oversees more than $1 trillion in assets, wrote directly to UK company chairs warning against the approval of excessive pay packages. The letter called for renewed discipline in executive remuneration, acknowledging that boards should retain flexibility to design competitive pay while emphasising the importance of the pay-for-performance principle. Fidelity highlighted two specific practices observed in the preceding year as particularly concerning: the de-risking of management incentives following poor performance, and the use of incentive structures built around insufficiently stretching hurdles. Fidelity’s letter reinforces a consistent message from the investor community that the pay-for-performance linkage will continue to be closely scrutinised, with votes used to signal discontent where company practices fall short.

Proxy Advisors’ Voting Guidelines

Having previously updated their guidelines to reflect the IA’s revised Principles of Remuneration, the major proxy advisory firms (ISS and Glass Lewis) made limited changes to their executive pay guidelines for 2026. ISS introduced one notable clarification: companies should provide a rationale and justification for the treatment of leavers in their remuneration report. Leaver treatment has historically been an area of investor concern in the UK, particularly where good leavers retain unvested awards, and this update adds an explicit disclosure expectation to an area that has sometimes lacked transparency. The clarification aligns with market best practice and reinforces a broader principle: that the link between pay and performance should hold not only during tenure but also at the point of executive departure.

Taken together, the guidance issued across the IA, Fidelity International, and the proxy advisors presented a coherent and mutually reinforcing set of expectations for the 2026 AGM season. Flexibility in pay design is accepted, but only where it is accompanied by compelling, transparent, company-specific justification and a demonstrable link between executive reward and performance.

Voting Outcomes – 2026

Remuneration Reports

As shown in Table 1, average support for remuneration reports has remained relatively stable over the past two years, though the proportion of companies facing significant dissent declined from 8.0% in 2025 to 5.4% in 2026. Strong market performance in 2025 contributed to a favourable voting environment, with the FTSE 350 and ISEQ 20 indices delivering returns of 24.1% and 37.4% respectively. As discussed before, pay-for-performance linkage is typically a core factor in investor voting decisions on remuneration, and strong market conditions generally lead to higher levels of approval (and pay). 11 companies, however, still recorded significant dissent on their remuneration report in 2026.

Table 1: Voting Statistics on Remuneration Reports – Based on Data from 1 January to 31 May Each Year

The most common sources of opposition in 2026, largely unchanged from last year, related to significant salary increases and committees failing to align pay outcomes with shareholder experience and company performance.

Among the 16 companies that received significant dissent in 2025, only four did so again in 2026, reflecting both the one-off nature of certain issues and the general tendency of UK and Irish boards to respond constructively to the signals sent by investors through their votes. Remuneration committee chairs who stood for re-election at companies that faced significant dissent over the past two years received between 17% and 37% of votes against their re-election, underscoring investors’ willingness to hold these directors accountable for continued shortcomings in remuneration practices.

Seven ‘new’ companies received significant dissent in 2026. While boards will at times need to take unconventional approaches to navigate market uncertainty, leadership transitions, or business transformation, annual reports should always seek to demonstrate clearly and in sufficient detail how such decisions align with shareholders’ interests.

Remuneration Policies

As shown in Table 2, average support for remuneration policies remained broadly stable over the past two years, though the proportion of companies receiving significant dissent declined from 11.1% in 2025 to 9.3% in 2026. This level of dissent nonetheless remains above that observed in 2023, when the majority of these companies last submitted their three-year remuneration policy for shareholder approval, signalling continued scrutiny of such proposals.

In addition, the gap in dissent between remuneration policies and remuneration reports is striking. Almost one in ten companies faced significant dissent on their remuneration policy in 2026, nearly double the proportion facing significant opposition on their remuneration report (5.4%). While strong market performance will have supported pay outcomes and dampened objections to remuneration reports, the growing shift toward hybrid LTIP structures among UK issuers contributed to sustain elevated dissent levels on remuneration policies.

Table 2: Voting Statistics on Remuneration Policies – Based on Data from 1 January to 31 May Each Year

Six of the seven instances of significant dissent on remuneration policies in 2025 related to the introduction of restricted shares combined with an overall increase in variable pay opportunity. In 2026, the drivers of significant dissent were more varied.

Out of the nine companies that attracted significant dissent in 2026, three faced such dissent as they sought approval to introduce restricted shares, despite applying a reduction in variable pay opportunity consistent with the 50% discount generally expected by investors. The remaining six sought significant variable pay opportunity increases using a range of different incentive structures.

In total, four companies seeking to introduce restricted shares in 2026 received significant dissent, continuing the trend observed in 2025. However, only one of these companies simultaneously sought to increase variable pay opportunity, suggesting a growing awareness of proxy advisor and investor expectations, and in particular the core expectation that companies apply a 50% discount to remuneration quantum when transitioning to restricted shares. That said, with three companies having applied this discount and still receiving significant dissent, it is clear that investors and proxy advisors scrutinise these arrangements beyond the quantum dimension alone. As a reminder we set out below the key expectations of IA members regarding the introduction of restricted shares as part of hybrid LTIP schemes.

IA Member Expectations: Hybrid LTIP Schemes

- Eligibility: Hybrid schemes should generally be reserved for companies that have a significant US footprint and/or compete for global talent.

- Rationale: Company rationales must go beyond generic statements and clearly explain how the proposed structure aligns with the company’s strategy, business model, and long-term success. Companies should explain why a hybrid model is preferred over a single structure.

- Early engagement: Remuneration committees are expected to consult with investors early when considering the implementation of a hybrid scheme.

- Discount rate: The restricted share portion of the hybrid scheme should be discounted to reflect its lower risk and higher certainty, typically by 50%, though a different rate may be appropriate depending on company circumstances. Companies should explain the rationale and methodology used to determine the discount rate.

- Underpins and discretion: Minimum performance underpins are expected to prevent vesting in circumstances of significant underperformance or as a result of events that put at risk shareholder returns. Discretion is expected to ensure there is no reward for failure.

- Vesting schedule: Annual vesting of restricted shares is generally not supported by shareholders.

Sources: Principles of Remuneration (October 2024), Letter to Remuneration Committee Chairs (November 2025).

Outlook

Shareholder meetings held to date in 2026 confirm that investors and proxy advisors continue to scrutinise remuneration proposals closely, with the linkage between pay and performance remaining central to how both remuneration reports and policies are assessed. As more UK companies adopt restricted shares as part of hybrid LTIP models, voting outcomes this season make clear that boards must develop a thorough understanding of investor expectations in the round, and not limit their focus to the question of quantum alone.

The environment in which remuneration decisions are being made has grown more complex. Geopolitical risk has emerged as a defining governance theme in 2026, driven partly by increased tensions in the Middle East but reflecting a broader pattern of global instability. For boards, the practical consequence is a harder task of designing incentive structures that effectively motivate senior leadership over the long term, attract and retain key talent, and maintain strong alignment with company performance and shareholders’ interests, all against a backdrop of heightened uncertainty. This is likely to sustain, and potentially accelerate, the adoption of restricted shares beyond their original purpose. While these schemes were initially introduced to help UK companies compete for talent with US peers, they are increasingly being considered by companies without significant global exposure, drawn by their retentive qualities in an uncertain market.

However, restricted shares are not the only lever available to boards navigating this environment. Companies may also consider other structural adjustments, including using metrics that emphasise strategic milestones or relative performance, revised performance measurement periods, or broader target ranges. Where such changes are made proactively, they are generally viewed more favourably by investors than recourse to ex-post board discretion.

The stakes of getting remuneration right extend beyond the AGM. Pay dissent gives third-party activists a credible platform from which to allege governance failure and rally other shareholders. To mitigate the risk of shareholder dissent, material changes should be discussed with key investors ahead of implementation and disclosed thoroughly in the following year’s annual report. Clear articulation of how remuneration decisions support the long-term creation of shareholder value will be essential. In an environment defined by uncertainty, companies that invest in early, substantive engagement with their key stakeholders will be best placed to maintain investor confidence, reduce their vulnerability to third-party intervention, and demonstrate that executive pay remains purposeful, proportionate, and aligned with the interests of those it is ultimately designed to serve.

The Team at FTI Consulting

In this complex and uncertain landscape, companies must prioritise designing remuneration structures that support their business objectives while satisfying diverse stakeholder expectations. FTI Consulting’s integrated team of reward specialists and communications professionals brings deep technical expertise in remuneration design, taxation, and governance, combined with a comprehensive understanding of the proxy advisory, stewardship, and activism landscape. We have a proven track record in helping companies develop robust remuneration programmes and achieve better outcomes through effective reporting and engagement. We partner with boards and management teams to navigate complex stakeholder dynamics and ensure pay practices align with strategic objectives while remaining publicly defensible.

The views expressed herein are those of the author(s) and not necessarily the views of FTI Consulting, Inc., its management, its subsidiaries, its affiliates, or its other professionals. FTI Consulting, Inc., including its subsidiaries and affiliates, is a consulting firm and is not a certified public accounting firm or a law firm.

FTI Consulting is an independent global business advisory firm dedicated to helping organisations manage change, mitigate risk and resolve disputes: financial, legal, operational, political & regulatory, reputational and transactional. FTI Consulting professionals, located in all major business centres throughout the world, work closely with clients to anticipate, illuminate and overcome complex business challenges and opportunities. © 2026 FTI Consulting, Inc. All rights reserved. fticonsulting.com