[1] Asociación de ISAPRES de Chile A.G. “ISAPRES 1981 – 2016: 35 years developing Chile’s private health system,” ISAPRE Trade Union Association 2016, https://www.isapre.cl/PDF/35YEARSIsapres.pdf.

[2] Id.

[3] Id.

[4] Id.

[5] Id.

[6] Id.

[7] “Estadísticas por tema,” Superintendencia de Salud de Chile (2023), https://www.supersalud.gob.cl/documentacion/666/w3-propertyvalue-3741.html.

[8] “Coldeco fusiona sus cuatro isapres para estandarizar el plan de salud de sus trabajadores,” CNN Chile (2020), https://www.cnnchile.com/economia/codelco-fusiona-isapres-plan-de-salud_20200215/.

[9] Matthew Malinowski and Eduardo Thomson, “Chile’s private health-care system is on verge of collapse, testing Boric,” BNN Bloomberg (2023), https://www.bnnbloomberg.ca/chile-s-private-health-care-system-is-on-verge-of-collapse-testing-boric-1.1893802.

[10] “ISAPRES 1981 – 2016: 35 years developing Chile’s private health system,” Asociación de ISAPRES de Chile A.G. (ISAPRE Trade Union Association 2016), https://www.isapre.cl/PDF/35YEARSIsapres.pdf.

[11] Id.

[12] “Estadísticas por tema,” Superintendencia de Salud de Chile (2023), https://www.supersalud.gob.cl/documentacion/666/w3-propertyvalue-3741.html.

[13] Franco Lopez, “Isapres informaron pérdidas a marzo por $2,152 millones en la previa de la presentación de ley corta,” BioBioChile (2023), https://www.biobiochile.cl/noticias/economia/negocios-y-empresas/2023/05/09/isapres-informaron-perdidas-a-marzo-por-2-152-millones-en-la-previa-de-la-presentacion-de-ley-corta.shtml.

[14] “Estadísticas por tema,” Superintendencia de Salud de Chile (2023), https://www.supersalud.gob.cl/documentacion/666/w3-propertyvalue-3741.html.

[15] “Chilean supreme court says Isapres can’t raise insurance premiums”, Bnamericas (January 2013), https://www.bnamericas.com/en/news/chilean-supreme-court-says-isapres-cant-raise-insurance-premiums.

[16] Matthew Malinowski and Eduardo Thomson, “Chile’s private health-care system is on verge of collapse, testing Boric,” BNN Bloomberg (2023), https://www.bnnbloomberg.ca/chile-s-private-health-care-system-is-on-verge-of-collapse-testing-boric-1.1893802.

[17] Eduardo Thompson, “UnitedHealth attacks Chile over new rules that fuel insurance crisis,” Bloomberg (2022), https://www.bloomberglinea.com/english/unitedhealth-attacks-chile-over-new-rules-that-fuel-insurance-crisis/.

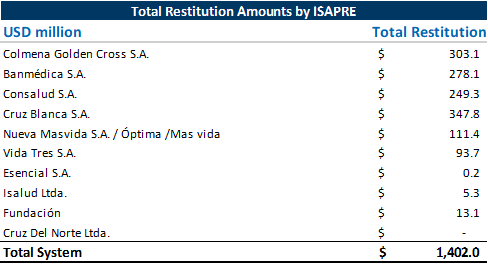

[18] Jorge Isla, “Ley corta: Gobierno confirma que las devoluciones de isapres bordean los US$ 1.400 millones,” Diario Financiero (2023), https://www.df.cl/empresas/salud/ley-corta-gobierno-confirma-que-las-devoluciones-de-isapres-bordean-los.

[19] “Encuesta Plaza Pública, Tercera Semana de Enero, Estudio 471,” Cadem Research & Estrategia (2023), https://cadem.cl/wp-content/uploads/2023/01/Track-PP-471-Enero-S3-VF.pdf.

[20] Cezary Wiśniewski and Ola Górska, “A need for preventative investment protection?,” Kluwer Arbitration Blog (2015), https://arbitrationblog.kluwerarbitration.com/2015/09/30/a-need-for-preventive-investment-protection/.

[21]Asociación de ISAPRES de Chile A.G., “ISAPRES 1981 – 2016: 35 years developing Chile’s private health system,” ISAPRE Trade Union Association (2016), https://www.isapre.cl/PDF/35YEARSIsapres.pdf.

[22] “Chilean supreme court says Isapres can’t raise insurance premiums”, Bnamericas (2013), https://www.bnamericas.com/en/news/chilean-supreme-court-says-isapres-cant-raise-insurance-premiums.

[23] MC2 Salud Healthcare Advisors, “Analysis of the Chilean healthcare (ISAPRE) sector in 2019,” MC2 Salud (2020), http://mc2salud.cl/estudios/MC2%20Salud%20-%20Analysis%20of%20the%20Chilean%20Healthcare%20(ISAPRE)%20Sector%20in%202019%20(07-Apr-2020).pdf.

[24] “Estadísticas por tema,” Superintendencia de Salud de Chile (2023), https://www.supersalud.gob.cl/documentacion/666/w3-propertyvalue-3741.html.

[25] MC2 Salud Healthcare Advisors, “Analysis of the Chilean healthcare (ISAPRE) sector in 2019,” MC2 Salud (2020), http://mc2salud.cl/estudios/MC2%20Salud%20-%20Analysis%20of%20the%20Chilean%20Healthcare%20(ISAPRE)%20Sector%20in%202019%20(07-Apr-2020).pdf.

[26] “Latin America insolvency regime scorecard,” Cleary Gottlieb (2020), https://www.clearygottlieb.com/-/media/files/emrj-materials/latin-america-insolvency-regime-scorecard-february-2020-update.pdf.

[27] Cristóbal Eyzaguirre B, Rodrigo Ochagavía R-T and Santiago Bravo S, “Chile,” Global Restructuring Review (2020), https://globalrestructuringreview.com/review/restructuring-review-of-the-americas/2021/article/chile.

[28] Jorge Isla, “Ley corta: Gobierno confirma que las devoluciones de isapres bordean los US$ 1.400 millones,” Diario Financiero (2023), https://www.df.cl/empresas/salud/ley-corta-gobierno-confirma-que-las-devoluciones-de-isapres-bordean-los.

[29] “Seguimiento de obras en ejecución decretadas y autorizadas,” Coordinador Eléctrico Nacional (2023). https://seguimientoejecucionobras.coordinador.cl/.

[30] Eduardo Thompson, “UnitedHealth attacks Chile over new rules that fuel insurance crisis,” Bloomberg (2022), https://www.bloomberglinea.com/english/unitedhealth-attacks-chile-over-new-rules-that-fuel-insurance-crisis/.

[31] For example, in 2013, the government of Slovakia proposed draft legislative reform which envisaged the creation of a single, state-run healthcare insurer, which would effectively squeeze out private health insurance providers including Achmea, a Dutch-based health insurer. Achmea filed a BIT claim, requesting – among other things – “to order the Slovak Republic to refrain from expropriating Achmea’s investment (Award on Jurisdiction and Admissibility of 20 May 2014, para. 96)”. The Tribunal found that Achmea had not demonstrated it had a prima facie case on the merits and, consequently, denied its jurisdiction, concluding that “it is not empowered to intervene in the democratic process of a sovereign State (Award on Jurisdiction and Admissibility of 20 May 2014, para. 251).”

Ana Heeren is a Senior Managing Director and the Head of Latin America for the Strategic Communications segment at FTI Consulting. She brings deep experience and a global perspective to her practice, having developed comprehensive communication plans, public relations strategies, issues and reputation management, and stakeholder engagements throughout Latin America, Europe and the United States. She was named to M&A Advisor’s Annual Emerging Leaders and Consulting magazine’s Rising Stars of the Profession lists in recognition for her work and creation of a multidisciplinary Latin America and Caribbean offering focused on the cross-border communications needs of corporates operating across the Americas.

Ana Heeren is a Senior Managing Director and the Head of Latin America for the Strategic Communications segment at FTI Consulting. She brings deep experience and a global perspective to her practice, having developed comprehensive communication plans, public relations strategies, issues and reputation management, and stakeholder engagements throughout Latin America, Europe and the United States. She was named to M&A Advisor’s Annual Emerging Leaders and Consulting magazine’s Rising Stars of the Profession lists in recognition for her work and creation of a multidisciplinary Latin America and Caribbean offering focused on the cross-border communications needs of corporates operating across the Americas.