Rough Seas or Calm Waters?

Amid evolving political dynamics, FTI forecasts LNG demand to almost double by 2040

U.S. liquefied natural gas (LNG) exports have grown exponentially since the first cargo left Sabine Pass in February 2016. While the COVID-19 pandemic caused a short-lived fall in mid-2020, export levels quickly rebounded by year’s-end—reaching a record average of 9.8 billion cubic feet per day (bcf/d) in December.

This incredible rise is owed to a variety of factors, including the availability of U.S. natural gas supply coupled with economic expansions and fuel switching in emerging markets, particularly Asia, global decarbonization policies, and geopolitics. Asian markets have accounted for 44 percent of U.S. LNG exports from February 2016 through November 2020, followed by 30 percent of cargoes to European nations, according to Department of Energy (DOE) data.

With the United States’ firm hold as the world’s top natural gas producer and an increasing focus of other nations seeking to solve the simultaneous economic growth and climate challenge, a clear opportunity exists for continued U.S. leadership in global LNG markets. While six LNG export facilities are presently online, the Federal Energy Regulatory Commission (FERC) has granted approval to twenty (20) additional facilities—a quarter of which are currently under construction—and is reviewing six (6) additional applications.

Amid a changing political landscape in Washington, market volatility, and global competition (i.e. Russia, Qatar, Australia), the 2021 U.S. LNG export outlook faces varying degrees of market uncertainty and regulatory risk—of which has historically been rough seas for the extractives sector. But navigating this uncertainty can be done through careful planning, forecasting, organizational commitment to Environmental, Social, and Governance (ESG) principles, and genuine stakeholder engagement.

LNG Market Outlook

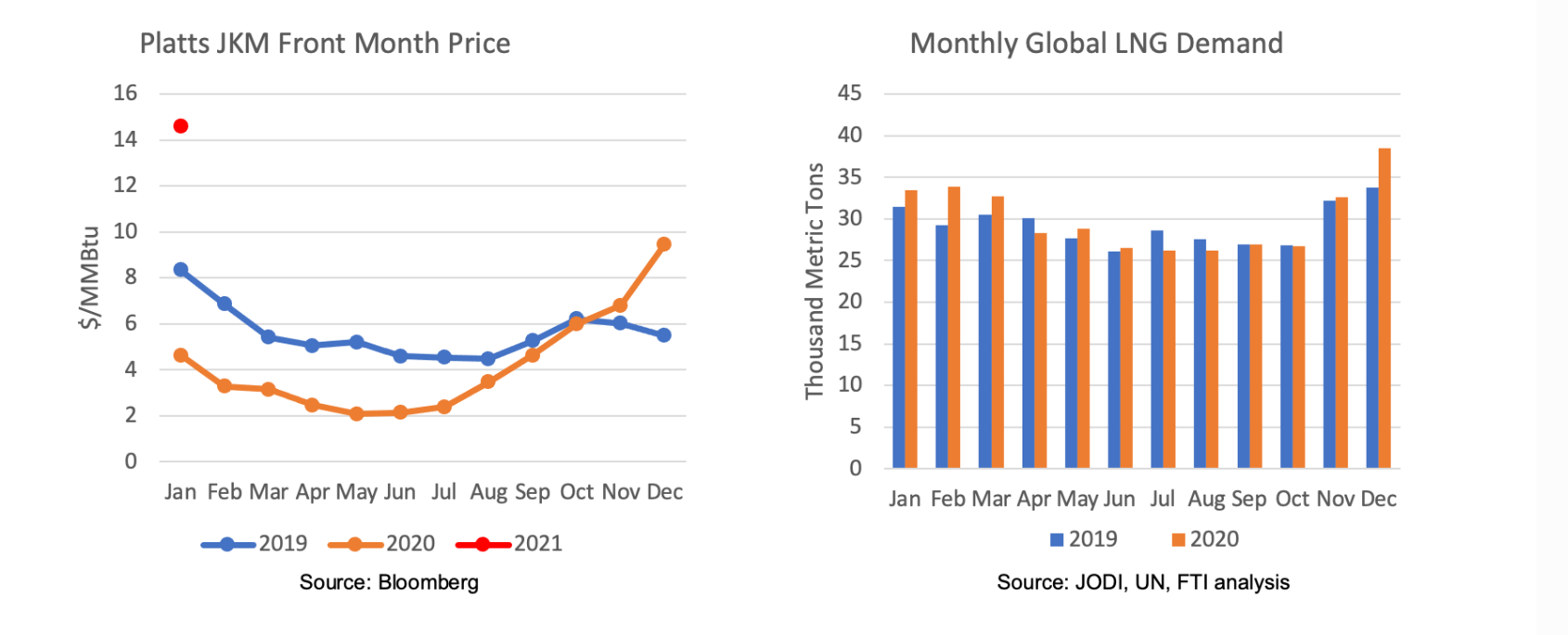

LNG markets have experienced significant volatility last year and early into 2021. January 2020 started on a soft note with the Platts Japan Korea Marker (JKM) front month price averaging $4.63/MMBtu – 44 percent below January 2019. COVID-19-induced lockdowns sharply decreased energy demand beginning in April and further exacerbated price declines. From April to November, monthly demands remained near or below 2019 monthly levels. By December 2020, appreciable cooling across the globe substantially raised LNG demand to a two-year monthly high of 38,000 metric tons. This cooler weather coupled with some liquefication outages led to a jump in JKM front month prices of almost $9.5/MMBtu, on average. This price rally extended into January 2021, with JKM front month prices averaging $14.58/MMBtu. In short, the last 13 months have been a rollercoaster for global LNG, with JKM front-month prices swinging from a daily low of $2.00/MMBtu to a daily high of $19.70/MMBtu.

On the supply side, only the U.S. added new export capacity in 2020 – around 20 million metric tons per annum (MTPA) or 2.7 bcf/d. On a high note for 2020, low LNG prices across the year buoyed demand for LNG in the face of a global recession, with 2020 demand slightly exceeding 2019 by 10 MTPA or 3 percent based on FTI’s estimate.

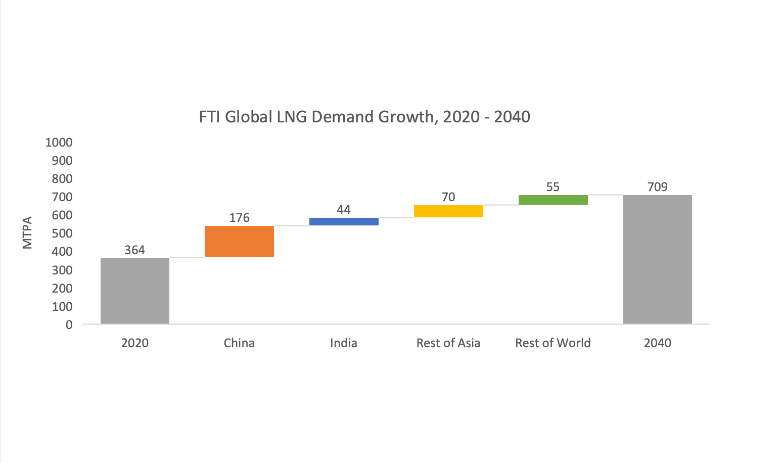

While price volatility will likely persist, in the mid-to-long term, global LNG demand will likely exhibit strong growth most notably due to the world’s decisive transition towards decarbonization alongside rising energy demand. FTI expects global LNG demand to increase from 345 MTPA in 2020 to 709 MTPA in 2040, with 51 percent of the increased demand coming from China, 13 percent from India, 20 percent from the rest of Asia, and the remaining 16 percent from the rest of the world.

Both China and India will likely lead the world’s regasification build-out, with each country planning to build dozens of new terminals by 2025. Notably, as China accelerates fuel switching and seeks to serve ever-growing energy demand, they will inevitably overtake Japan as the world’s top LNG importer. Domestic production and pipeline imports from Russia through the Power of Siberia pipeline will simply not be enough.

In India, rising industrial sector demand and declining domestic production, as well as a focus on curbing carbon emissions from coal, will spur additional LNG imports. While Indian LNG imports are likely to show more price sensitivity, and hinge on the timely buildout of pipeline networks connecting the ports to inland demand centers, India is poised to show tremendous growth in LNG imports in the medium to long term.

Japan and Korea, the traditional Asian LNG-importing powerhouses, along with most of Europe will experience flat LNG demand growth due to net zero commitments.

The U.S. is well-positioned to meet the global growth in LNG demand. With its four under-construction projects, twenty FERC-approved projects, and six additional liquefaction projects under consideration, the U.S. could supply up to 245 MTPA or 71 percent of the expected 345 MTPA of incremental LNG demand by 2040.

Shifting U.S. Policy Outlook

The rapid ascension of U.S. LNG exports largely occurred under the Trump administration, who viewed the fuel a critical component to its “energy dominance” strategy. Key government leaders touted the economic, environmental, and geopolitical benefits of U.S. energy exports, with former Energy Secretary Rick Perry describing LNG as “freedom gas.”

Political winds in Washington have shifted, though, as the incoming Biden administration and subsequent Democratic control of Congress will bring about a marked policy change, driven largely by a starkly different ideological view on how to fuel the country. For his part, President Biden has walked a tight rope on energy, environment, and climate policy. While the former Vice President dismissed calls to ban hydraulic fracturing and rejected the proposed Green New Deal, favored by more the more progressive win of the Democratic Party, he has signaled that aggressive climate action will be a key federal policy area. Still, substantive policies can largely be gleaned by a historical trajectory.

Campaign policy positions (i.e., net-zero emissions by 2050), cabinet nominations (Jennifer Granholm for Energy Secretary) and White House policy advisors (John Kerry as Climate Envoy, Gina McCarthy as White House climate czar) offer an early look into the Biden administration’s likely aggressive climate action and regulatory waves to come. While it’s unlikely we’ll hear former Gov. Granholm touting “freedom gas,” the likely incoming Energy Secretary said during her confirmation hearing that she believes LNG has “an important role to play” in reducing GHG emissions.

Still, reports on President Biden, who was a proponent of LNG exports during the Obama administration, characterize his plans for the oil and gas sector as “evasive” and “murky.”

There is no doubt that such policy voids cast a serious shadow of regulatory uncertainty for companies invested—or considering investments—in the U.S. The unknown potential of project delays is real, particularly a given the highly regulated nature of the sector and the role the federal government plays in the life cycle of any size or type of venture. At FERC, the primary oversight agency, Democrat Richard Glick is the new chair, but Republicans will hold a 3-2 majority until Commissioner Chatterjee’s term expires in June and President Biden can appoint a new Democrat commissioner. In various dissents regarding LNG export approvals, Glick has been critical, repeatedly citing the agency’s “refusal to consider the consequences its actions have for climate change.”

But LNG could also align closely with the Biden administration’s priorities: LNG is a cornerstone to the global energy transition, enjoys broad union building trades support, lowers the U.S. trade deficit, considered a key foreign diplomacy tool, and carries environmental benefits compared to other forms of energy production and consumption.

Thus, a political priority shift does not guarantee a dimmed prospect of additional U.S. LNG export terminals. Rather, companies that demonstrate best-in-class operations and core commitments to ESG principles, will be well-positioned in gaining and maintaining investment capital, capturing market share, and securing needed regulatory approvals.

Navigating Regulatory Risk, Uncertainty

The emergence of robust ESG reporting and action appeared prior to the change in the White House. Driven by public and investor sentiment, effective ESG frameworks – which are measurable and clearly reflect an organization’s values, including guidance from critical internal and external stakeholders – must be fundamental to business objectives and the thesis of any investment opportunity.

These expectations apply to all companies; but the spotlight shines increasingly so on those in the energy sector. Companies with effective programs can proactively communicate their positions and objectives to ensure the business case remains achievable and persuasive. Increasingly so, these external, largely non-technical factors are critical risk factors that must be properly managed. Put another way, they are existential.

Consider, for example, the French utility, Engie, terminated a twenty-year, $7 billion contract to import U.S. LNG last year, because investors and French government estimated methane emissions didn’t align with the utility’s climate goals. Engie is just one case study to attempt to understand how a Biden administration—and increasingly the capital markets community—will likely approach energy infrastructure projects. It also exemplifies how managing these risks can be accomplished through genuine stakeholder and community engagement; effective, action-oriented ESG reporting; and demonstrating the value of achieving low-carbon policies:

- Effective, Action-Oriented ESG Framework: Organization-wide commitments to ESG frameworks are no longer simply accoutrements. Shifting public, government and financial community expectations has driven change in company behavior and a refreshed vision on what “good” corporate citizenship looks like. Clearly measurable, performance based ESG frameworks are “corporate table stakes,” as colleagues recently wrote. It is nearly a guaranteed prophecy that LNG operators who are ESG leaders will be best positioned for success.

- Genuine Stakeholder, Community Engagement: The community and stakeholders around a company (and their assets) are a critical component or organization success. It is critical that companies recognize the importance and develop a community and stakeholder engagement strategy that engages with key community leaders, finds opportunities for partnership, and shows tangible, shared value. Most importantly, the engagement strategy will—and should—evolve over time. As our society continues to confront existing and new challenges, companies with an evolve strategic approach can rise to any occasion. Issues like environmental justice will continue to present an ever-present threat and opportunity to companies of all sizes.

- Demonstrate Value in Low-Carbon Policies: As countries work towards meeting the Paris Climate Accords targets, domestic LNG will play a key role in decarbonizing power grids and industrial sectors. Securing market share in a low-carbon future, requires both sustainable operations, thoughtful, pragmatic political engagement, and effective story telling. The United States’ ability to continue its leadership in LNG space can coexist with America’s ability to deliver consistent energy security to many nations around the globe who are moving away from coal-dominated energy mixes.

As the world progresses through the ongoing energy transition towards a low-carbon future, the market opportunities for U.S. LNG remain a critically important element in the endeavor. Securing broad recognition and managing non-technical regulatory and political risks requires thoughtful planning and commitment. It will be those companies willing to engage in thoughtful and proactive dialogues that are able to show value and fortitude able to overcome the roughest of risk seas or the calmest market waters.